The optionality characteristic of options results in a non-linear payoff for options. In simple words, it means that the losses for the buyer of an option are limited, however the profits are potentially unlimited. For a writer (seller), the payoff is exactly the opposite. His profits are limited to the option premium, however his losses are potentially unlimited. These nonlinear payoffs are fascinating as they lend themselves to be used to generate various payoffs by using combinations of options and the underlying. We look here at the six basic payoffs (pay close attention to these pay-offs, since all the strategies in the book are derived out of these basic payoffs).

1.2.1 Payoff profile of buyer of asset: Long asset In this basic position, an investor buys the underlying asset, ABC Ltd. shares for instance, for Rs. 2220, and sells it at a future date at an unknown price, St. Once it is purchased, the investor is said to be “long” the asset. Figure 1.1 shows the payoff for a long position on ABC Ltd.

Figure 1.1 Payoff for investor who went Long ABC Ltd. at Rs. 2220

The figure shows the profits/losses from a long position on ABC Ltd.. The investor bought ABC Ltd. at Rs. 2220. If the share price goes up, he profits. If the share price falls he loses.

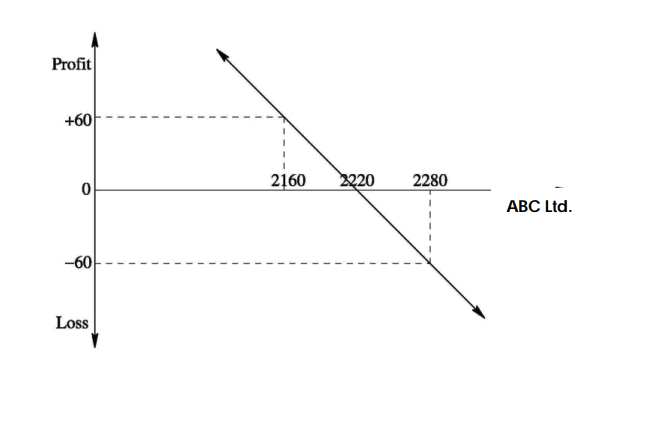

1.2.2 Payoff profile for seller of asset: Short asset In this basic position, an investor shorts the underlying asset, ABC Ltd. shares for instance, for Rs. 2220, and buys it back at a future date at an unknown price, St. Once it is sold, the investor is said to be “short” the asset. Figure 1.2 shows the payoff for a short position on ABC Ltd.

Figure 1.2 Payoff for investor who went Short ABC Ltd. at Rs. 2220

The figure shows the profits/losses from a short position on ABC Ltd.. The investor sold ABC Ltd. at Rs. 2220. If the share price falls, he profits. If the share price rises, he loses.

1.2.3 Payoff profile for buyer of call options: Long call A call option gives the buyer the right to buy the underlying asset at the strike price specified in the option. The profit/loss that the buyer makes on the option depends on the spot price of the underlying. If upon expiration, the spot price exceeds the strike price, he makes a profit. Higher the spot price, more is the profit he makes. If the spot price of the underlying is less than the strike price, he lets his option expire un-exercised. His loss in this case is the premium he paid for buying the option. Figure 1.3 gives the payoff for the buyer of a three month call option (often referred to as long call) with a strike of 2250 bought at a premium of 86.60.

Figure 1.3 Payoff for buyer of call option

The figure shows the profits/losses for the buyer of a three-month Nifty 2250 call option. As can be seen, as the spot Nifty rises, the call option is in-the-money. If upon expiration, Nifty closes above the strike of 2250, the buyer would exercise his option and profit to the extent of the difference between the Nifty-close and the strike price. The profits possible on this option are potentially unlimited. However if Nifty falls below the strike of 2250, he lets the option expire. His losses are limited to the extent of the premium he paid for buying the option.

1.2.4 Payoff profile for writer (seller) of call options: Short call A call option gives the buyer the right to buy the underlying asset at the strike price specified in the option. For selling the option, the writer of the option charges a premium. The profit/loss that the buyer makes on the option depends on the spot price of the underlying. Whatever is the buyer’s profit is the seller’s loss. If upon expiration, the spot price exceeds the strike price, the buyer will exercise the option on the writer. Hence as the spot price increases the writer of the option starts making losses. Higher the spot price, more is the loss he makes. If upon expiration the spot price of the underlying is less than the strike price, the buyer lets his option expire un-exercised and the writer gets to keep the premium. Figure 1.4 gives the payoff for the writer of a three month call option (often referred to as short call) with a strike of 2250 sold at a premium of 86.60.

Figure 1.4 Payoff for writer of call option

The figure shows the profits/losses for the seller of a three-month Nifty 2250 call option. As the spot Nifty rises, the call option is in-the-money and the writer starts making losses. If upon expiration, Nifty closes above the strike of 2250, the buyer would exercise his option on the writer who would suffer a loss to the extent of the difference between the Nifty-close and the strike price. The loss that can be incurred by the writer of the option is potentially unlimited, whereas the maximum profit is limited to the extent of the up-front option premium of Rs.86.60 charged by him.

1.2.5 Payoff profile for buyer of put options: Long put A put option gives the buyer the right to sell the underlying asset at the strike price specified in the option. The profit/loss that the buyer makes on the option depends on the spot price of the underlying. If upon expiration, the spot price is below the strike price, he makes a profit. Lower the spot price, more is the profit he makes. If the spot price of the underlying is higher than the strike price, he lets his option expire un-exercised. His loss in this case is the premium he paid for buying the option. Figure 1.5 gives the payoff for the buyer of a three month put option (often referred to as long put) with a strike of 2250 bought at a premium of 61.70.

Figure 1.5 Payoff for buyer of put option

The figure shows the profits/losses for the buyer of a three-month Nifty 2250 put option. As can be seen, as the spot Nifty falls, the put option is in-the-money. If upon expiration, Nifty closes below the strike of 2250, the buyer would exercise his option and profit to the extent of the difference between the strike price and Nifty-close. The profits possible on this option can be as high as the strike price. However if Nifty rises above the strike of 2250, he lets the option expire. His losses are limited to the extent of the premium he paid for buying the option.

1.2.6 Payoff profile for writer (seller) of put options: Short put A put option gives the buyer the right to sell the underlying asset at the strike price specified in the option. For selling the option, the writer of the option charges a premium. The profit/loss that the buyer makes on the option depends on the spot price of the underlying. Whatever is the buyer’s profit is the seller’s loss. If upon expiration, the spot price happens to be below the strike price, the buyer will exercise the option on the writer. If upon expiration the spot price of the underlying is more than the strike price, the buyer lets his option un-exercised and the writer gets to keep the premium. Figure 1.6 gives the payoff for the writer of a three month put option (often referred to as short put) with a strike of 2250 sold at a premium of 61.70.

Figure 1.6 Payoff for writer of put option

The figure shows the profits/losses for the seller of a three-month Nifty 2250 put option. As the spot Nifty falls, the put option is in-the-money and the writer starts making losses. If upon expiration, Nifty closes below the strike of 2250, the buyer would exercise his option on the writer who would suffer a loss to the extent of the difference between the strike price and Nifty close. The loss that can be incurred by the writer of the option is a maximum extent of the strike price (Since the worst that can happen is that the asset price can fall to zero) whereas the maximum profit is limited to the extent of the up-front option premium of Rs.61.70 charged by him.